Navigating a crisis: How the 2023 cash scarcity shaped household consumption in Ondo State, Nigeria

Abstract

Economic history frequently reveals how societies tolerate and adjust during financial crises. The year 2023 was critical for Nigeria due to severe cash scarcity, which went beyond inconvenience and significantly upset citizens’ daily lives. In an increasingly digital and cashless economy, shortages of physical currency raise dire concerns about household consumption behavior. This study examines the effects of cash scarcity on spending patterns, financial behavior, savings, and the adoption of alternative payment methods among Nigerian households. The study used primary data collected from 180 respondents and employed statistical tools such as frequency and percentage distributions, tables, charts, mean statistics, and correlation analysis. The findings reveal that cash scarcity affected the consumption behavior of a significant proportion (88.9%) of respondents, altering spending patterns and limiting the ability to meet essential needs. Major factors contributing to the scarcity included inflation (mean = 3.52), political instability (mean = 3.13), counterfeiting (mean = 3.11), and challenges within the banking sector (mean = 3.09). Results further indicate that 75.0% of households experienced reduced savings and investment, while 92.8% reported increased reliance on alternative payment methods, leading to heightened financial stress. Common coping strategies adopted by households included reducing non-essential spending (72.8%) and modifying shopping habits (60.6%), with only 1.7% reporting no impact. The study underscores the importance of effective currency management and responsive fiscal and monetary policies. It recommends targeted social interventions, investment in digital financial infrastructure, flexible budgetary frameworks, inflation control measures, and regulatory reforms within the banking sector. Promoting financial inclusion, particularly in rural areas, is essential to ensure resilience during similar crises. Overall, the study highlights the need for coordinated policies to mitigate the immediate effects of cash scarcity while fostering long-term economic stability.

Introduction

Nigeria, often referred to as the "Giant of Africa," has a rich economic history characterized by both promising growth and significant challenges (Sohn, 2020). Its journey from independence in 1960 to the present has seen various economic phases and transitions. Following independence, Nigeria experienced strong economic growth during the 1960s and 1970s, largely driven by the discovery of oil in the Niger Delta and the oil boom of the 1970s (Thomas et al., 2022). While oil revenues generated unprecedented wealth, they also entrenched overdependence on oil, corruption, and weak economic diversification (Ezeogidi, 2020). The volatility of global oil prices exposed Nigeria to recurrent economic shocks, notably during the 1980s oil glut, which resulted in fiscal deficits and economic contraction (Rasheed, 2023). Structural Adjustment Programs introduced in the late 1980s sought economic reform but imposed significant social costs on citizens. The return to democratic governance in 1999 renewed optimism for economic stability, supported by reforms and growth in sectors such as telecommunications (Lueders, 2024). However, political instability, corruption, and regional unrest persisted. Banking sector crises in the 1980s and 1990s revealed deep systemic weaknesses, prompting comprehensive reforms including bank recapitalization, stricter regulation, enhanced supervision, and deposit insurance through the Nigeria Deposit Insurance Corporation (Azétsop et al., 2020). These reforms strengthened financial resilience, encouraged foreign participation, and restored confidence in the banking system.

A major turning point occurred with the fuel subsidy removal in 2012, which triggered nationwide protests and economic disruption (Isyaku and Hamza, 2023). While intended to reduce fiscal burdens and redirect funds toward development, the policy led to sharp increases in fuel prices, inflation, and cost of living pressures (Abubakar et al., 2023). Although a partial subsidy was reinstated after public outcry, the episode intensified debates on governance, fiscal responsibility, and accountability. Nigeria faced another severe challenge during the 2016–2017 recession, driven primarily by declining oil prices, structural inefficiencies, and limited economic diversification (Yamoah, 2023). The recession led to GDP contraction, rising inflation, and increased unemployment. Concurrently, a currency crisis caused significant depreciation of the naira, escalating import costs and reducing purchasing power. Policy responses included exchange rate controls, fiscal austerity, and efforts to diversify the economy, though the effects lingered beyond the recession (Matallah, 2022).

The 2023 cash scarcity marked a recent and transformative economic episode, characterized by shortages of physical currency amid a growing shift toward digital finance (Ghana, 2023). Banking infrastructure challenges, currency management issues, and broader economic instability intensified the crisis. Households adapted by embracing electronic payments, altering spending and savings behaviors, and relying more on digital platforms. While this accelerated financial innovation, it also exposed vulnerabilities within the informal economy. In this era of increasingly digital and cashless economies, the scarcity of physical currency raised pivotal questions about the dynamics of household consumption behavior in the face of such adversity (Naeem, 2023). This research embarks on an exploration of the multifaceted landscape shaped by the 2023 cash scarcity in Nigeria, seeking to shed light on its causes, consequences, and the strategies adopted by households to navigate this challenging terrain. The aim is to discern how the scarcity of cash influenced not only the spending patterns of households but also their broader financial behaviors, from savings practices to the adoption of alternative payment methods (Li et al., 2021). Through a comprehensive analysis, we seek to offer insights into the unique economic realities that unfolded during this period and their enduring impacts on the financial behaviors of Nigerian households.

The significance of this research extends beyond its immediate empirical contribution. The 2023 cash scarcity was not merely an economic event but also a profound social and institutional challenge that disrupted livelihoods, altered financial practices, and accelerated Nigeria’s transition toward digital financial systems (Otame, 2023; Akata, 2022). Understanding household responses to this crisis offers valuable insights into adaptive capacity, vulnerability, and resilience in developing economies. Moreover, the findings provide critical evidence for policymakers, financial institutions, and development practitioners seeking to design effective social protection mechanisms, strengthen financial inclusion, enhance regulatory frameworks, and improve crisis-response strategies. For businesses and financial service providers, insights into changing consumption patterns and payment preferences offer guidance for strategic planning, service innovation, and product development.

By situating household behavior within the broader context of macroeconomic instability, financial sector reform, and digital transformation, this study contributes to the growing body of literature on economic shocks and household welfare in emerging economies. It bridges a critical gap by offering empirical evidence from Nigeria’s 2023 cash scarcity, thereby enriching scholarly discourse on financial resilience, consumption adaptation, and crisis management.

The broad objective of this study is to assess the effects of the 2023 cash scarcity on households’ consumption behavior in Ondo State, Nigeria. The specific objectives are to:

(i) examine the extent of the 2023 cash scarcity on household consumption behavior;

(ii) analyze the factors contributing to the cash scarcity;

(iii) investigate the effects of cash scarcity on household consumption patterns and financial behavior; and

(iv) explore the coping strategies adopted by households during the cash scarcity period.

Material and Methods

Study population and sampling technique

The population of this study is comprised of households in Ondo State, Nigeria. A multi-stage sampling technique was used for this study, giving rise to a total sampling size of one hundred and eighty (180) respondents.

Source of data

Data for this study was collected through the use of a well-structured questionnaire.

Data analytical techniques

Data were analyzed using frequency, percentage, table, charts, mean statistics, and correlation analysis.

Results and Discussion

Extent of the cash scarcity of 2023 on households’ consumption behavior

Awareness of respondents about cash scarcity of 2023

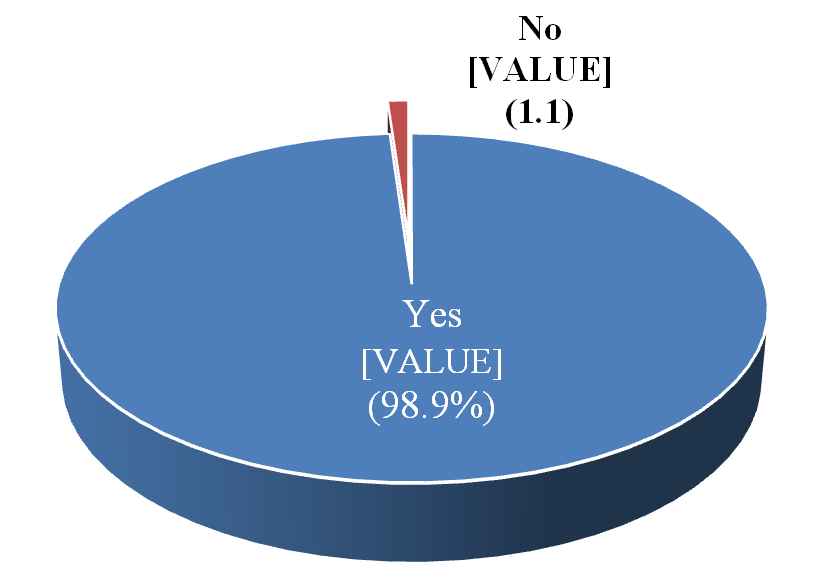

According to the statistics shown in Fig. 1, 98.9% of respondents were aware of the nationwide cash scarcity problem that occurred in Nigeria in 2023. The pervasive effects of the cash shortage are highlighted by this high awareness rate. It implies that this problem had a major impact on the people of Ondo State, Nigeria. This high level of awareness draws attention to how serious the situation was and how it could affect people's ability to support themselves and their businesses. These results are in line with those of Ani et al., 2024, who found that 97.9% of participants knew about the cash shortage and the redesign policy.

Fig. 1: Percentage distribution of respondents on awareness of respondents about cash scarcity of 2023

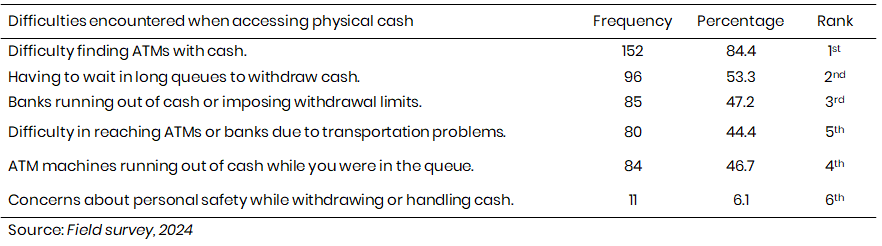

Challenges/difficulties encountered when accessing physical cash during the cash scarcity period

The results in Table 1 show that the respondents identified and ranked the difficulty in finding ATMs with cash (84.4%) as the most significant challenge experienced in the study area. "Having to wait in long queues to withdraw cash" (53.3%) was the second-ranked problem. Respondents noted that the major frustrations during this period were the long queues and extended waiting times at banks or ATMs to access cash. Banks imposing withdrawal limitations or running out of cash (47.2%) was another major difficulty. Many respondents highlighted that the withdrawal and transaction thresholds set by the banks were particularly challenging. The worry for one's personal safety when handling or withdrawing cash came in last on the list of challenges (6.1%). This indicates that safety concerns were not a major issue for respondents, possibly because they were withdrawing less cash and thus were less worried about security threats associated with cash handling.

Effect of the cash scarcity of 2023 on households’ consumption behavior

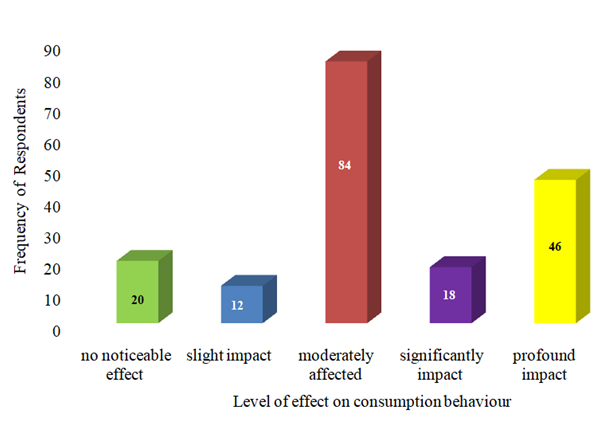

The findings displayed in Fig. 2 demonstrate that a sizable segment of participants (46.7%) concurred that their consumption pattern was somewhat impacted by cash scarcity, necessitating certain modifications. Furthermore, 25.6% of respondents said that the lack of cash had a significant influence on their purchasing habits, leading to significant adjustments and difficulties. This implies that the respondents' purchasing patterns were significantly impacted by the cash scarcity, most likely as a result of their dependence on cash to cover everyday expenses.

On the other hand, 10.0% of the participants stated that the lack of cash had a substantial influence on their consuming habits, leading to considerable modifications. 11.1% of respondents claimed the event had no discernible impact on their consumption habits, while 6.7% reported a minor but manageable impact.

Fig. 2: Percentage distribution of respondents on perceived level of effect of Cash Scarcity of 2023 on household consumption beha

Effect of the cash scarcity of 2023 on households’ spending pattern

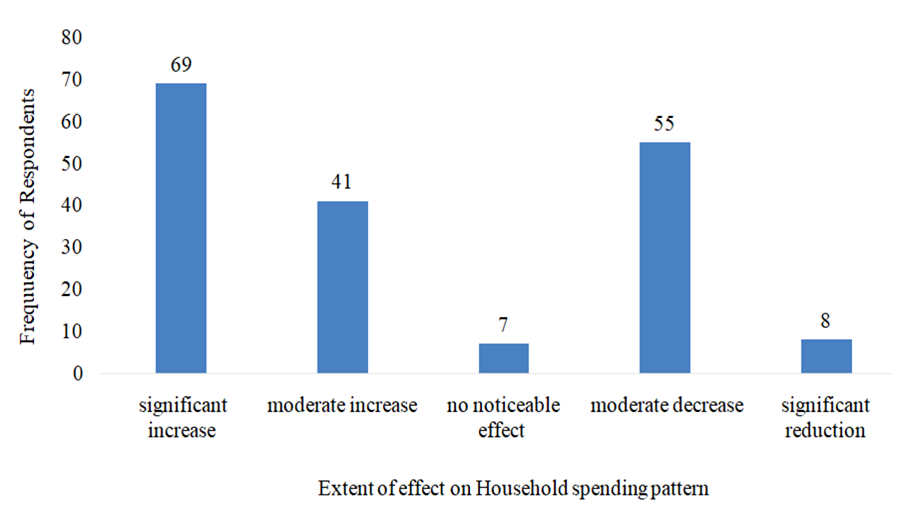

The results shown in Fig. 3 indicate that a substantial number of respondents (38.3%) agreed that the cash shortage led to a significant increase in their household spending due to higher prices or increased expenses, while 22.8% reported a moderate increase in household spending as a result of the cash dearth. Additionally, 30.6% believed that the cash scarcity led to a moderate decrease in their household spending as they adjusted their expenses.

This implies that the scarcity noticeably affected the spending patterns of the respondents, causing various adjustments and changes in how they managed their finances, especially given the challenges of accessing cash during this period.

Furthermore, 4.4% of the respondents reported that their household spending was significantly reduced, and only 3.9% claimed that the currency scarcity had no noticeable effect on their spending patterns.

These findings clearly indicate that the cash scarcity event in 2023 had varying impacts, both positive and negative, on the households in the study area.

Fig. 3: Percentage distribution of respondents on perceived level of effect of Cash Scarcity of

Table 1: Challenges/difficulties encountered when accessing physical cash during the cash scarcity period

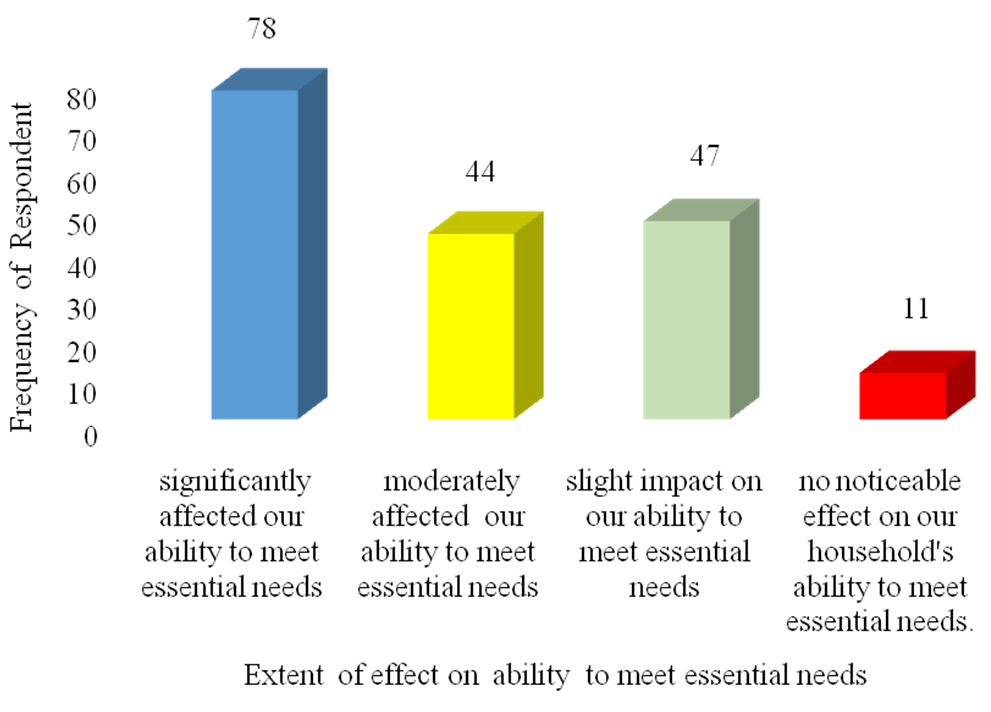

Effect of the cash scarcity of 2023 on households’ ability to meet essential needs

Furthermore, Fig. 4 illustrates the various effects that the cash scarcity in 2023 had on households' ability to meet basic needs. The results showed that the statement "the cash scarcity significantly affected our ability to meet essential needs, leading to major challenges in accessing food, healthcare, or education" was the most agreed upon, with 43.3% of respondents supporting it. Additionally, 24.4% of respondents admitted that their ability to meet essential needs was moderately affected due to the cash scarcity, resulting in some difficulties.

These findings clearly demonstrate that the cash scarcity caused significant hardship and stress for Nigerian residents, particularly in accessing basic and essential needs such as food and healthcare. The limited or constrained access to cash, coupled with some outlets and stores demanding payment in cash only, greatly impacted their ability to meet these essential needs.

Fig. 4: Percentage distribution of respondents on perceived level of effect of Cash Scarcity of 2023 on ability to meet essential

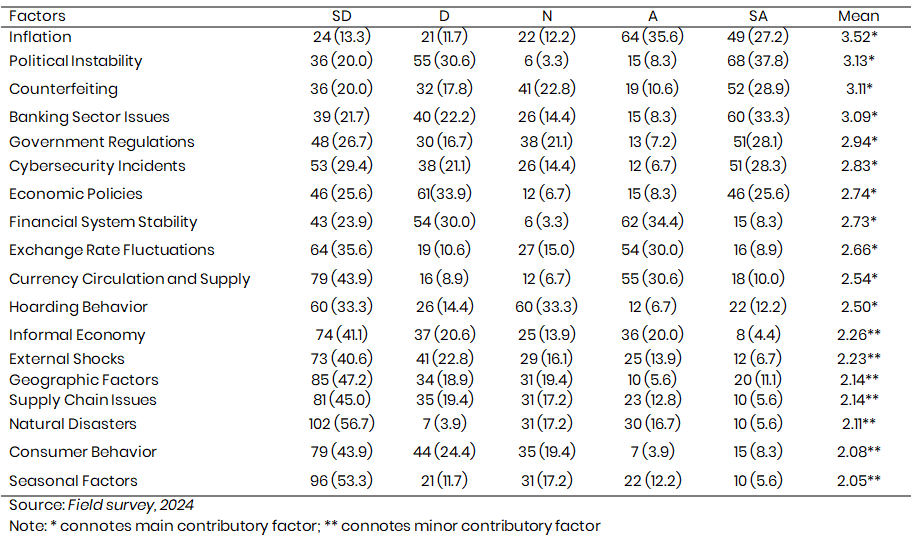

Factors contributing to the cash scarcity of 2023

The opinions of the respondents regarding the several issues they believe have contributed to the cash scarcity in 2023 are displayed in Table 2. All respondents agreed that the primary cause was inflation (x̅ = 3.52). This implies that the public believes that a significant contributing factor to the cash scarcity is the inflation of goods and services. Because it was an election year, the political atmosphere in the nation during this time probably contributed to the significant perception that political instability was the second largest factor (x̅ = 3.13). Many conjectured that Nigerian political deals played a role in the cash shortage, bolstering the claim made by Akinlo et al. (2022) that there is a direct and adverse correlation between political instability and economic growth in Nigeria. This is also consistent with the finding of Adamaagashi et al. (2023) that there is a direct correlation between political conflict and economic inequality, where economic inequality is defined as differences in wealth, income, and assets between various persons or groups.

Counterfeiting (x̅ = 3.11) and problems with the banking system (x̅ = 3.09) were two other causes that were found to be significant drivers of cash scarcity in 2023. This emphasizes how decision-makers and financial systems influenced the incident, highlighting the indisputable shortcomings and difficulties these parties faced during the cash scarcity situation.

Table 2: Factors contributing to the cash scarcity of 2023

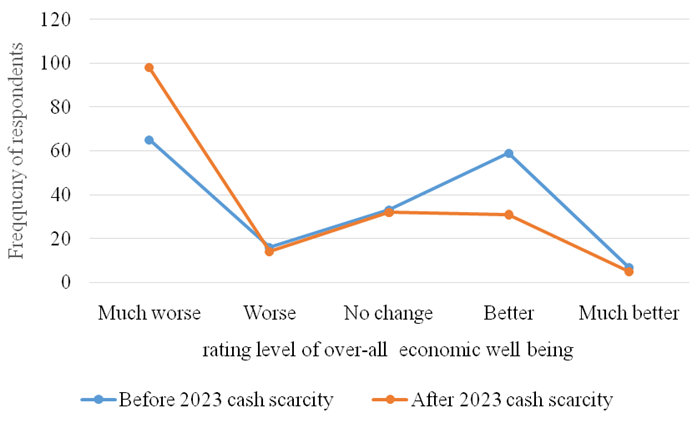

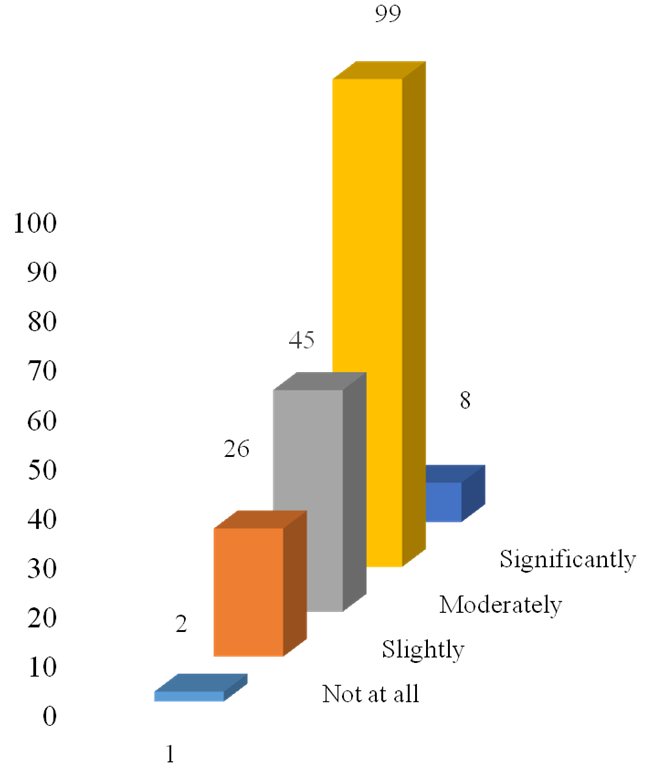

Perceived overall rating of household’s economic wellbeing before and after the 2023 cash scarcity

The respondents' assessments of their household's financial well-being before and after the cash scarcity event of 2023 are contrasted in Fig. 5. The findings indicate a substantial disparity in the evaluations, with almost 100 participants asserting that their financial security was significantly worse following the incident, in contrast to 65 who assessed it as significantly worse before the incident. Given that the respondents experienced considerable hardship during this time due to limited access to cash, it appears that the cash scarcity had a large detrimental effect on their financial wellness. The proportion of respondents who thought their economic welfare was better before the cash scarcity (35 respondents) and those who thought it was better after the cash scarcity (51 respondents) also differed noticeably. The fact that a small percentage of respondents said they felt their economic wellbeing had increased after the event suggests that some people were able to use adaptive tactics to get through the challenging time and keep or even improve their economic wellbeing in spite of the national crisis.

Fig. 5: Perceived overall rating of household’s economic wellbeing before and after the 2023 cash scarcity

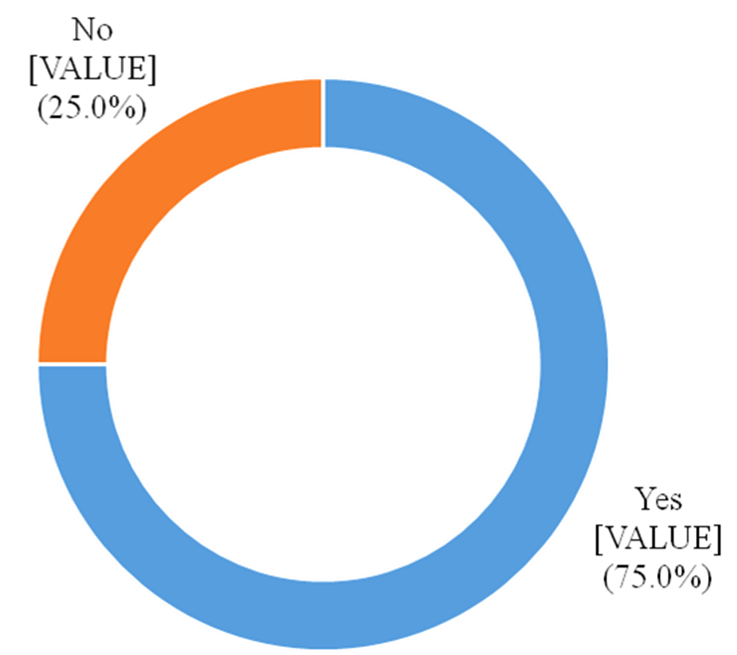

Cash scarcity influence on household's savings and investment strategies

The majority of respondents (75.0%) agreed that cash scarcity affected their household savings and investment strategies, according to the results shown in Fig. 6. This implies a connection between financial decisions on investments, savings, and cash availability. These results are consistent with those of Lingyan et al. (2021), who discovered that cash availability, or financial accessibility, is a significant indicator that has an impact on private investment and its linked control variables in both positive and negative ways.

Fig. 6: Did the cash scarcity influence your household's savings and investment strategies?

Utilization of alternative payment methods, such as mobile money or electronic transfers, during the cash scarcity

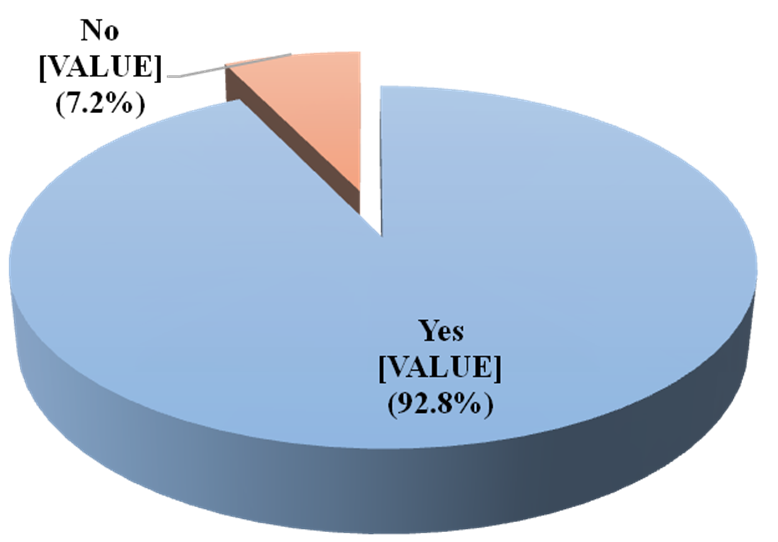

During the cash shortage, the majority of respondents (92.8%) stated that they made use of other payment methods, including electronic transfers or mobile money (Fig. 7). This suggests that, at the time, the populace relied on alternate payment methods, including bank apps, mobile money, and e-channels. Interviews, however, indicated that this tactic only somewhat reduced the challenges brought on by the scarcity. Certain retailers and service providers mandated cash payments due to their inability to wait for confirmation delays resulting from financial institutions or network problems.

Fig. 7: Percentage distribution of respondents based on utilization of alternative payment methods, such as mobile money or electr

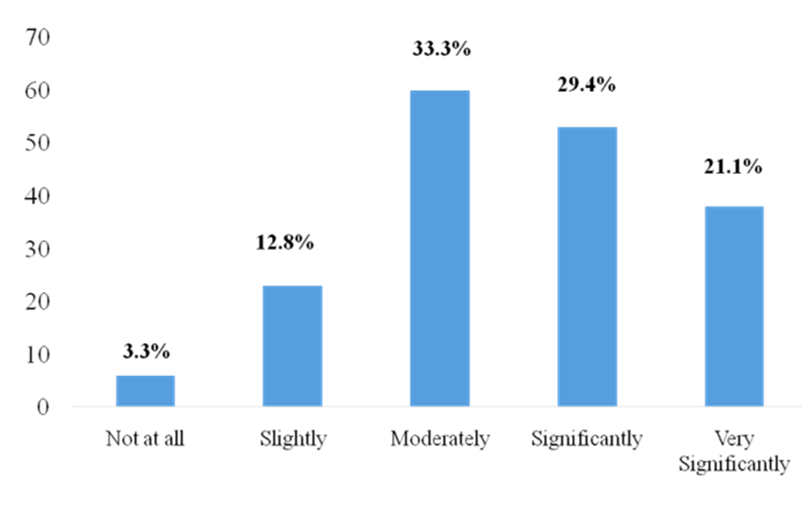

The degree to which the cash shortage generated financial stress within homes was examined to further investigate how it affected households in the study area. According to the results, while 29.4% and 21.1% of respondents said that cash scarcity had a major and very substantial financial burden on their households, respectively, 33.3% of respondents agreed that it created moderate financial stress. 3.3% of respondents stated they did not experience any financial hardship as a result of the cash constraint, while the remaining few respondents (12.8%) stated it had a minor impact (Fig. 8). This finding indicates that 84.8% of the households polled were highly impacted by cash scarcity, with 50.5% reporting significant to very significant stress. Implications include, potentially unstable economic conditions, decreased consumption, and heightened vulnerability among affected households.

Fig. 8: Distribution of respondents by levels of financial stress faced within household due to cash scarcity

Average monthly estimated household expenditures by categories

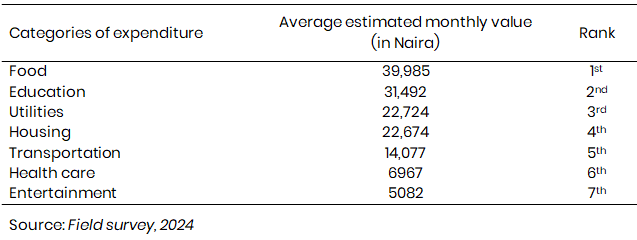

The result in Table 3 shows that the respondents had spending on food as the highest ranked expenditure (₦39,985) they make in their households, while expenditures on education were ranked second with an average estimation of ₦31,492 monthly. Then closely linked to these two highly ranked expenditures were: utilities (₦22,724), housing (₦22,674), and transportation (₦14,0477). Households prioritize spending on food and education in Ondo State, Nigeria, indicating a commitment to human capital and fundamental needs. The significant expenditures for housing, transportation, and utilities, however, highlight other necessary costs. Insufficient funds might put access to utilities and education at risk, increasing financial stress and impeding socioeconomic growth. This would call for focused actions to lessen the negative consequences for livelihoods.

Table 3: Average monthly estimated household expenditures by categories

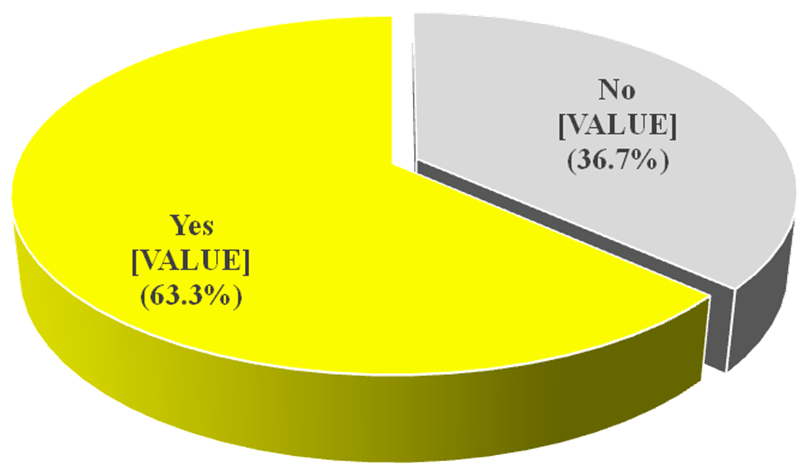

The results in Fig. 9 show that many (63.3%) of the respondents agreed that they experienced a change in their household spending behavior. This suggests a discernible change in the way their households spend their money. This result is consistent with that of Gomes et al. (2021), who also noted variations in respondents' spending habits.

Fig. 9: Perceived change in household's spending behavior

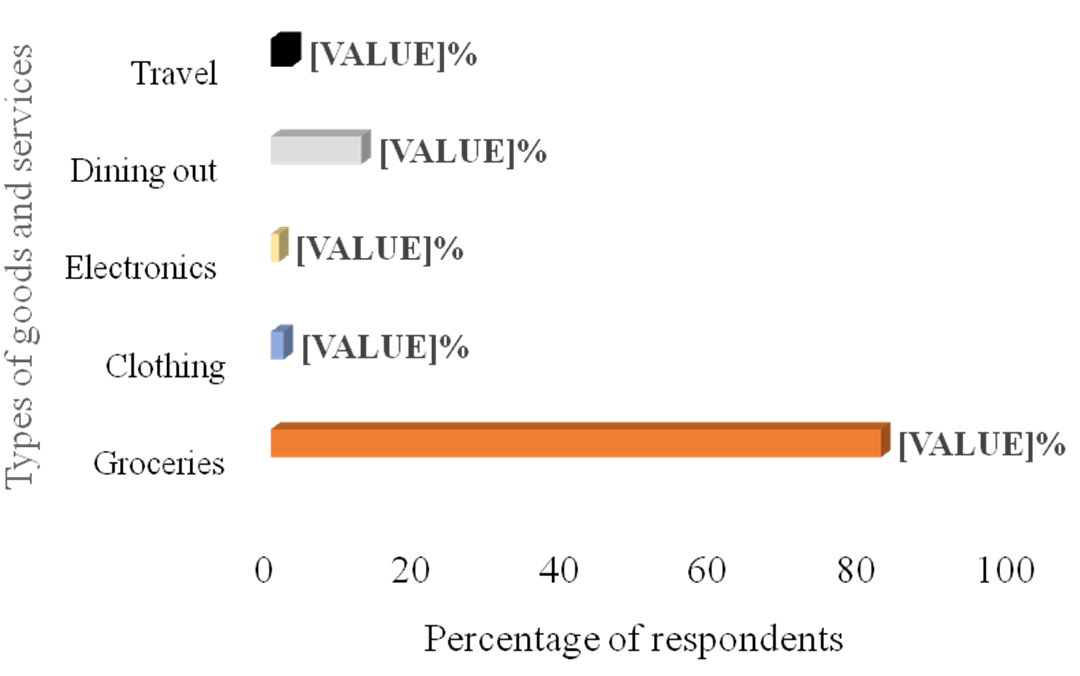

The types of goods and services that your household typically purchases regularly

The research indicates that a majority (82.2%) of respondents spend their income on groceries. This implies that respondents prioritize spending on groceries, suggesting a fundamental emphasis on sustenance. This focus potentially leaves little room for other essential expenses or savings. Cash scarcity may exacerbate challenges in accessing nutritious food, leading to food insecurity and impacting overall household well-being and health (Fig. 10).

Fig. 10: Percentage distribution of respondents by the types of good and services households typically purchase regularly

Extent of external factors (such as economic conditions or policy changes) impact on household's consumption behavior

The results in Fig. 11 indicate that 55.0% of respondents agreed that external factors significantly impact household consumption behavior, 25.0% felt the impact of external factors moderately, and 14.4% claimed that external factors like economic policies and policy changes have only a slight impact on their household consumption. Additionally, 4.4% of respondents believed external factors had a very significant impact, while only 1.2% claimed they had no impact at all.

Fig. 11: Frequency distribution of respondents by their level of perceived impact of external factors on household&r

This implies that external factors, such as economic policy, affect household consumption in various ways, as 98.8% of respondents acknowledged feeling its impact, ranging from slight to very significant. These findings support those of Kim et al. (2021), who found a strong negative association between economic policy uncertainty and household consumption, particularly in areas such as food, transportation, communication, entertainment, and social interaction expenses. The results also align with Madudova and Corejova's (2023) opinion that household consumption expenditure is a crucial measure of economic activity, reflecting the spending behavior of households and their purchasing power.

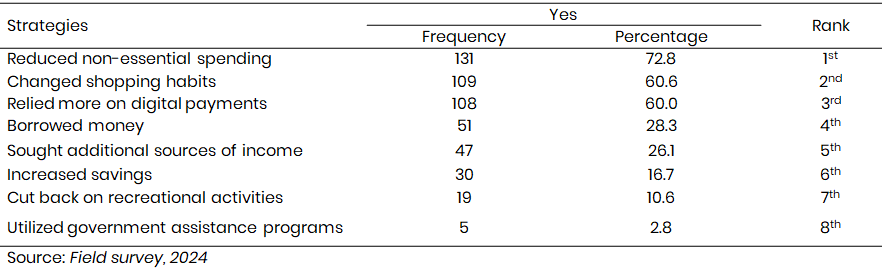

Strategies employed to cope with the cash scarcity of 2023

The results in Table 4 reveal the strategies respondents used to cope with cash scarcity in 2023. It shows that 72.8% of respondents primarily reduced non-essential spending to lessen the impact of cash scarcity on their households and wellbeing. This indicates that respondents developed the habit of prioritizing essential needs and making opportunity-cost decisions.

A similar strategy that ranked second was changing shopping habits and frequency due to limited cash access. Additionally, 60.0% of respondents relied on digital payments to reduce the impact of cash scarcity on their households. This reliance on digital payments highlights the adaptation to available alternatives when cash is scarce.

Table 4: Ranking of the strategies employed to cope with the Cash Scarcity of 2023

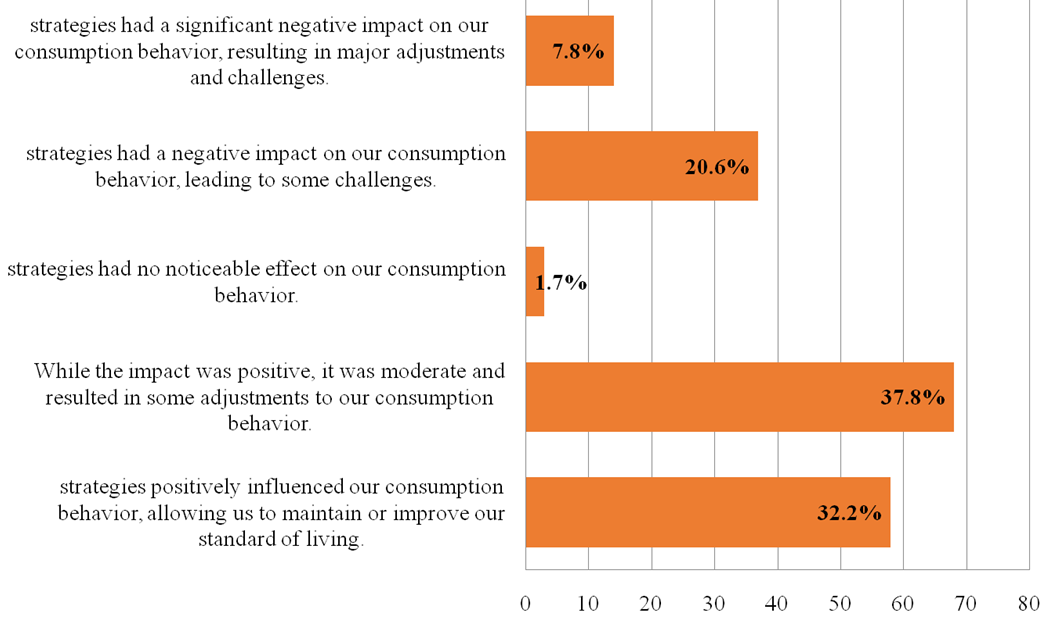

Effect of adopted strategies on the household consumption behavior

The results show that 37.8% of respondents reported that the strategies they adopted had a positive but moderate impact, resulting in some adjustments to their consumption behavior. Additionally, 32.2% agreed that the strategies they utilized positively influenced their consumption behavior, allowing them to maintain or improve their standard of living. This implies that the majority (70.0%) of respondents claimed that the strategies they adopted to combat the cash scarcity challenge in 2023 had a positive impact on their consumption patterns, helping them adapt and survive the hardship. However, a smaller percentage (28.4%) of respondents indicated that the strategies they used to cope with cash scarcity had a negative impact on their households. This could be due to a lack of capacity or resilience to effectively address the challenge or the use of unsuitable strategies, such as borrowing money they cannot repay, leading to negative effects on their household consumption behavior (Fig. 12).

Fig. 12: Percentage distribution of respondents by effect of adopted strategies on the household consumption behavior

Conclusion

The study provides empirical information on the assessment of the effects of the 2023 cash scarcity on household consumption behavior. Results showed that the cash scarcity had a noticeable effect on household consumption patterns and spending, causing significant financial stress. It indicated that political instability, inflation, and issues within the banking sector were contributory factors to this national crisis in 2023. The study also revealed that the majority of respondents devised several strategies to cope with the cash scarcity, with these strategies having varying degrees of effectiveness on their households and livelihoods. Additionally, the period witnessed widespread use of alternative payment methods, especially mobile payments and electronic channels, by the Nigerian populace. This adaptation highlights the resilience and resourcefulness of households in navigating economic challenges.

To mitigate these issues, the study suggests that Fiscal policies should include targeted social interventions, such as direct cash transfers or subsidies, to alleviate the immediate financial burdens on vulnerable populations. Increased focus on digital infrastructure investment to enhance alternative payment methods and reduce dependency on physical cash. This could be prioritized in government budgets to support smoother transitions during similar crises. There is a need for fiscal policies that provide flexibility in budget allocations to respond swiftly to crises like cash scarcity. This includes emergency funds that can be quickly mobilized to support households and stabilize the economy. The study underscores the critical role of effective currency management. The Central Bank of Nigeria (CBN) needs to ensure adequate circulation of physical currency while promoting digital payment systems to prevent cash shortages. With inflation identified as a key factor contributing to cash scarcity, monetary policies must prioritize controlling inflation. This involves managing interest rates and employing other monetary tools to stabilize prices. Regulatory reforms aimed at improving the efficiency and resilience of the banking sector are essential. This includes ensuring banks are equipped to handle increased digital transactions and crises. Increased reliance on alternative payment methods during times of cash scarcity indicates a shift towards digital finance. Policies should aim at promoting financial inclusion, ensuring that all demographics, especially those in rural areas, have access to digital financial services. The study underscores the need for robust and responsive fiscal and monetary policies that address the immediate impacts of cash scarcity while promoting long-term economic stability and growth.

References

Abubakar, O. A., Audu, A. A., & Goyilla, A. E. (2023). An assessment of socio-economic effects of fuel subsidy removal in Nigeria. Theme.

Adamaagashi, I., Bello, K., Nwimo, C., & Collins, O. (2023). The intersection of economic inequality and political conflict in Africa: A comprehensive analysis. International Journal of Social Sciences and Management Research, 9, 1–33.

Akata, D. (2022). The effect of COVID-19 on electronic currencies as they become common payment methods. In Pandemnomics: The pandemic's lasting economic effects (pp. 221–237). Springer Nature Singapore.

Akinlo, T., Arowolo, O. H., & Zubair, T. B. (2022). Political instability and economic growth in Nigeria. Review of Socio-Economic Perspectives, 7(2), 47–58.

Ani, J. I., Ajayi-Ojo, V. O., & Batisai, K. (2024). Financial scarcity, psychological well-being and perceptions: An evaluation of the Nigerian currency redesign policy outcomes. BMC Public Health, 24(1), 1164. https://doi.org/10.1186 /s12889-024-1164

Copyright

Open Access: This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.